LFP electric vehicle battery adoption hits fresh record

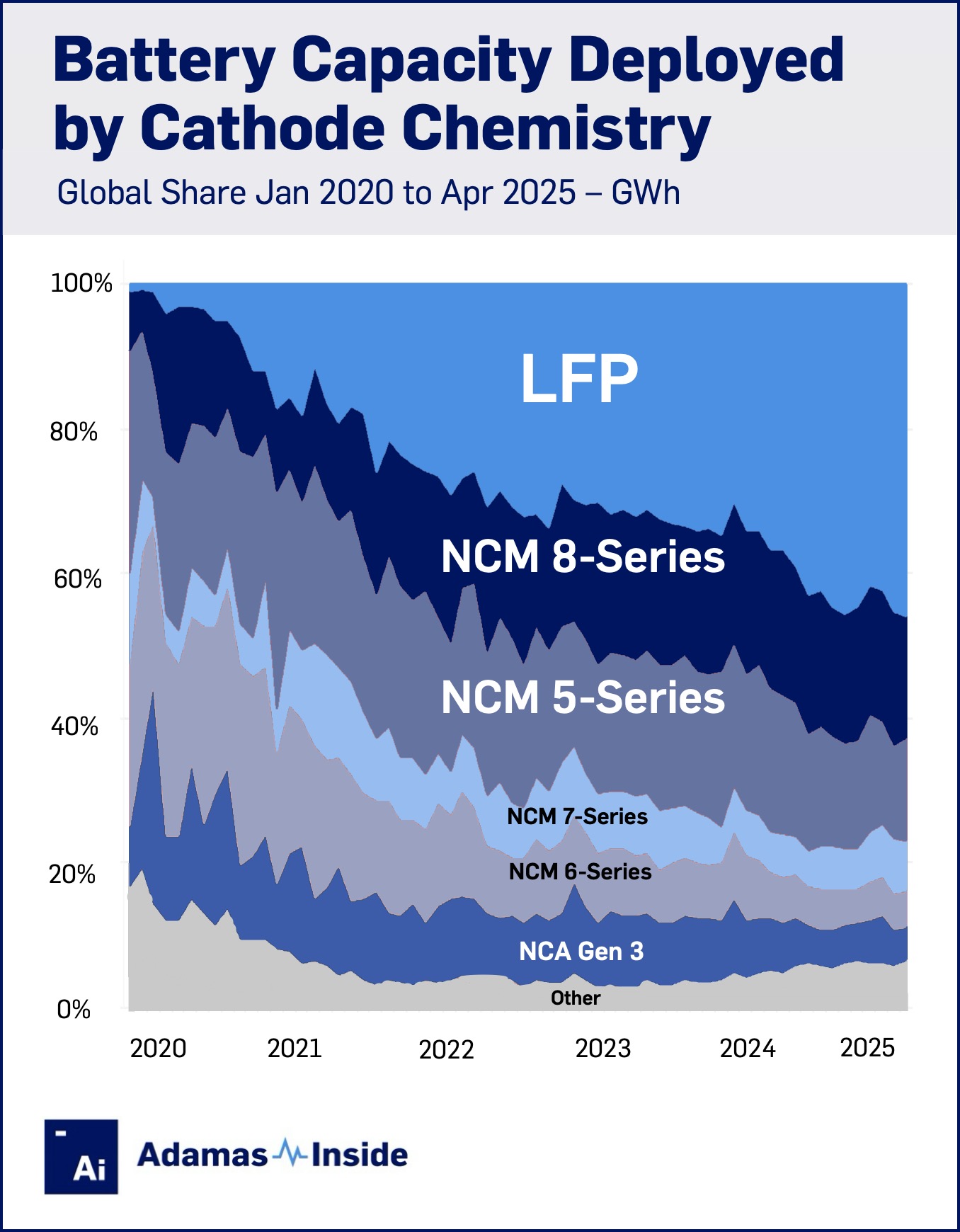

Global penetration of EVs powered by lithium iron phosphate batteries sped to a new monthly record of 46% on a capacity deployed basis in April this year.

The combined capacity of LFP packs deployed in newly sold EVs during the month hit 35.6 GWh after surging by 76% year on year.

From powering a limited number of low end, compact cars and utility vehicles, LFP adoption kicked into high gear in early 2020. The catalysts were BYD’s introduction of the so-called Blade prismatic battery pack and conversion of its entire model line-up to the cathode chemistry, and Tesla starting shipments of entry level LFP models from its Shanghai factory.

Fast forward to today and on a cumulative basis, a third of the battery capacity installed since then has been in EVs equipped with LFP packs.

A full 84% or 29.8 GWh of the April total were rolled onto roads in China where the cathode chemistry now commands two thirds of the market. April’s top contributors to LFP adoption in the country were the base model of Xiaomi’s SU7 and the new Geely Xingyuan subcompact hatch which pushed the latest version of the Model Y into third place.

Among the world’s largest EV markets, France, Germany and the UK showed the fastest expansion for the cathode with all three countries seeing a doubling of LFP capacity deployed compared to April 2024, albeit from a low base.

The new Ford Explorer SUV made for the European market which sports an LFP pack supplied by CATL led the charge on the continent with the imported BYD Seal coming in second.

On the European market, LFP constituted 9% on a GWh basis in April as Chinese imports more than make up for a sharp pullback in Tesla Model Y and Model 3 sales on the continent.

In the Americas, year-on-year growth was a more sedate 20%, dragged down by a shrinking LFP tireprint in the US despite rapid expansion elsewhere, including in Canada, where deployment increased by 101% and Mexico (+188%).

The LFP-powered versions of Tesla’s two workhorses account for 37% of LFP deployment in the region where overall adoption of the nickel and cobalt-free battery has now entered double digits on a percentage basis.

As an indication of Chinese automakers uneven ability to expand in the region, LFP penetration goes from 70% in Brazil to only 5% in the US.