CHART: Cellphones on wheels

Calling electric cars cellphones on wheels – often disparagingly – has become something of a cliche in the industry.

But there is more than a little truth to it.

Carplay

To the delight of shareholders and the disappointment of aficionados, Apple extinguished its not-so-secret EV ambitions a year ago.

Chinese counterpart Xiaomi tread where Cupertino feared and entered automaking in a spectacular fashion, barely a couple of months after Project Titan was tanked.

But the link between cellphone makers and electric cars goes back to the early years of the industry.

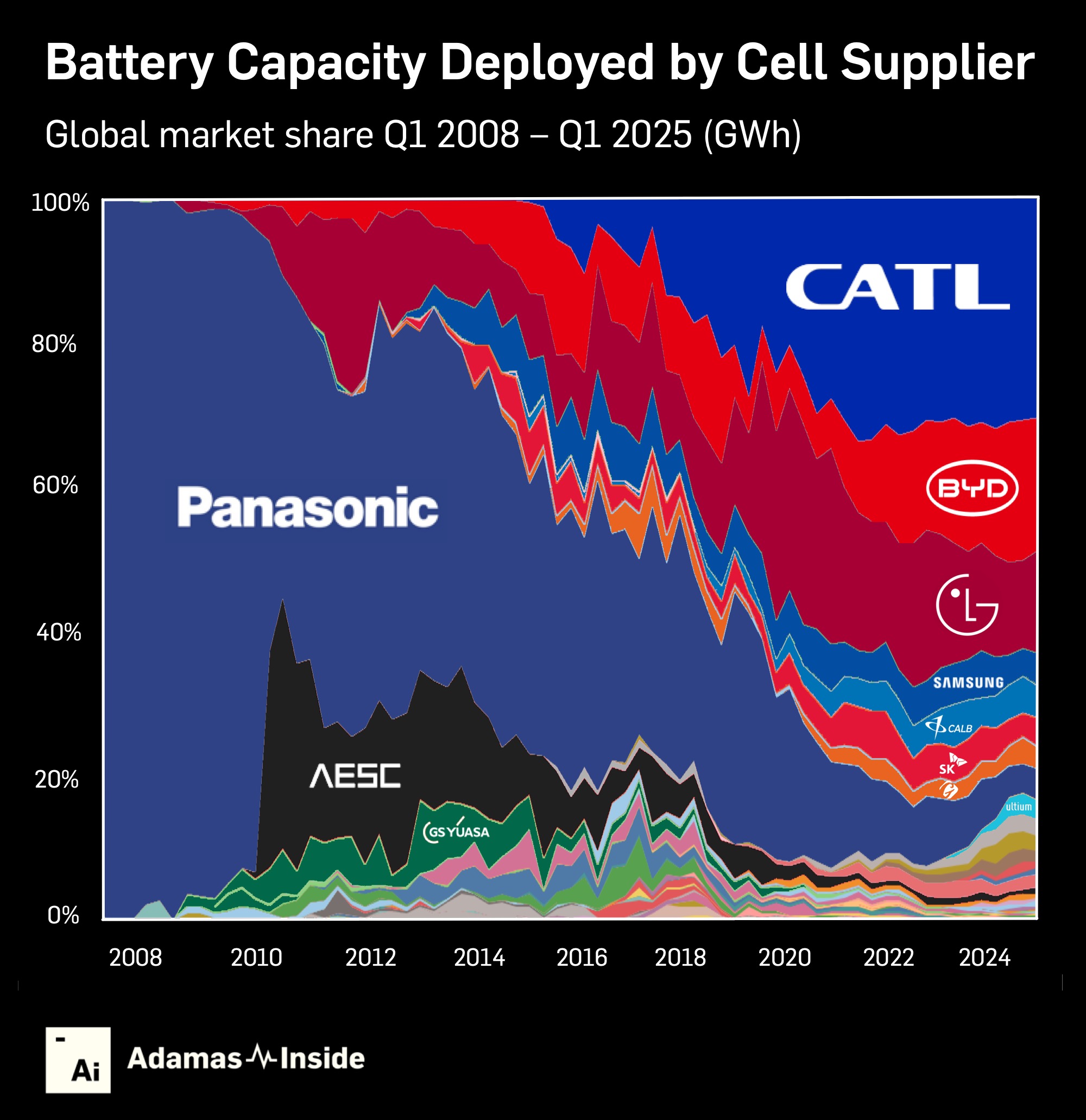

The graph displays the market share of EV cell suppliers from the first quarter of 2008 up to and including Q1 2025 on a battery capacity deployed basis using our EV Battery Intel Platform (which goes all the way back to 2004).

Triple As

Tesla’s first model, the Roadster, was launched in February 2008 but the EV world back then was an old-school hybrid affair, specifically the Toyota Prius and its nickel metal hydride battery supplier Panasonic.

But if you needed a reminder of what a different world that was, consider this:

It was not until 2010 that the combined battery capacity of all EVs sold annually exceeded 1 GWh. More than double that figure hits the global roads each and every day. And 2025 is almost certain to be the first terawatt calendar year.

Until 2024, Tesla was the top EV maker on a battery capacity deployed basis, fending off competition from legacy automakers’ belated assault on the market and scores of startups, mainly in China.

For battery makers, however, the landscape changed dramatically and rapidly in the intervening years.

Panasonic was able to hold onto its near monopoly on the industry for a few years, thanks to its NCA pack partnership with Tesla.

Fast forward to Q1 2025 and the Japanese company’s share of the market is down to a paltry 4% on a GWh basis.

And to get back to the analogy, Panasonic still makes cellphones. Just not smartphones.

Leaving money on the table

Another Japanese firm Automotive Energy Supply Corporation or AESC along with its progenitor also squandered their first mover advantage.

AESC began life as a Nissan joint venture installing batteries in the Leaf, invariably called the world’s first mass market EV by those who think the TH!NK City is an urban planning app.

AESC was able to capitalize on the greenfield Leaf project and by Q2 2011 had cornered 35% of the market on a combined battery capacity deployed basis.

At the time it must have appeared that AESC would live up to its corporate title, but today the Yokohama company’s automotive energy supply constitutes less than 1% of the global total. It’s also wholly owned by a Chinese battery concern.

Android auto

LG Chem, now LG Energy Solution, enjoyed its largest corner of the market in Q3 2012 at just about a quarter after capitalizing on the Chevy Volt.

Unlike its peers across the Sea of Japan, the Korean conglomerate has been able to hold onto a large chunk of its early position and sits comfortably as the number three EV cell supplier in total GWh terms.

LG stopped making new cellphones in 2021 and at the end of this month will stop all software updates.

Like any chaebol worth its salt Samsung also got into the EV game early, teaming up with BMW on the German automaker’s ugly duckling, the i3, more than a decade ago (the i3 like the first Volt was an EREV, but that’s another story).

Samsung’s global market share in cellphones peaked in the second half of 2012 at nearly a third. Around the same time, it mastered roughly 8% of the EV battery market. On both counts Samsung’s slice has now been cut almost in half.

Contemporaries

CATL, in just over a decade, has become the undisputed leader in EV battery making and in good quarters can capture up to a third of the market.

Picking up the call from Xiaomi to provide the power packs for its top of the range Porsche killers helps as does all the business it picked up from Tesla as the Texas company’s Panasonic relationship narrows.

Before adding Contemporary to its name and switching to EVs, Amperex Technology Co was a provider of cellphone batteries – just like BYD.

The world’s top electric carmaker – and only integrated electrified OEM – entered the market when Panasonic looked untouchable.

In 2025, as a cell supplier (also to a handful of other makes including Xiaomi’s LFP entry level models) it reigns over nearly a fifth of the market in GWh terms.

Highway

Perhaps the ultimate example of cellphones on wheels is Huawei.

The telecoms giant supplies software, including battery management systems, to 11 EV makers, and created marketing and development relationship with some of China’s top EV brands including Luxeed, AITO, Avatr and Trumpchi.

Apple is in a bear grip with its stock trading down more than 20% year to date as its once buzzy cellphone business runs out of juice.

Apple needs to show the world it can still invent great products and perhaps an iCar (too late, Chery already has it trademarked) may well be back on the drawing board.

After all, the last 17 years have shown you can make a cellphone on wheels.