Global car parc electrification growth stays above 30%

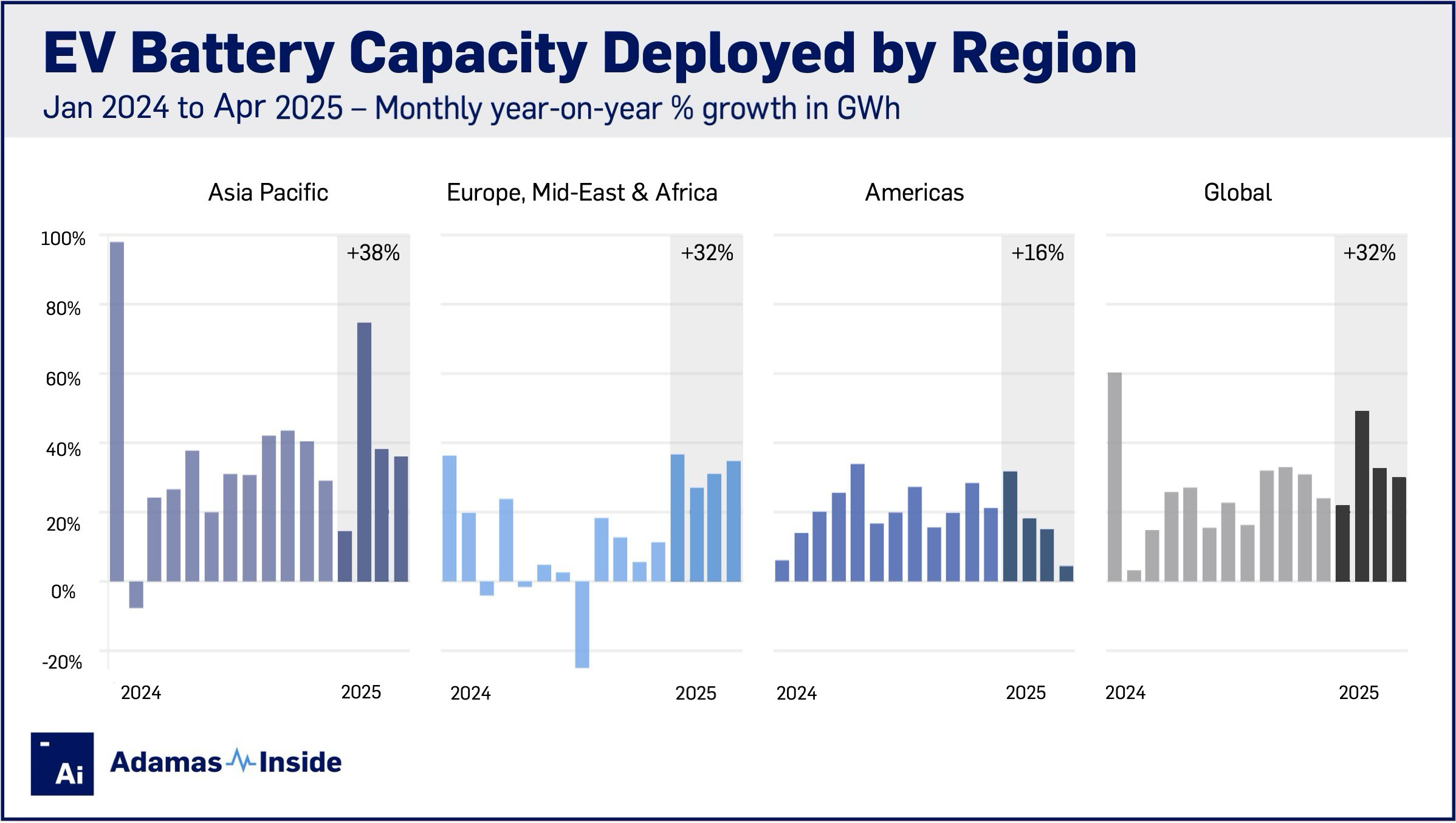

During the first four months of 2025, 291.7 GWh of battery capacity was deployed onto roads globally in all newly sold passenger EVs combined, 32% more than the same period last year.

Even with a commanding 61% share of the global market, Asia Pacific added fresh capacity at more than double the rate (+38% year over year) compared to the Americas.

After a strong start to 2025, growth in the Americas – where the US and Canada make up 90% of the market – fell to the lowest in several years in April at less than 5% year on year. Year-to-date regional growth now clocks in at 16% over 2024.

From January through April, new EVs in the US added 13% more battery capacity to the nation’s roads. In Canada, new EVs increased battery capacity by 28%, while in Mexico, it surged by 156% to 1.2 GWh closing the gap to Brazil which after a torrid 2024 is now stationary.

After a choppy 2024, Europe continues to accelerate with the market expanding by 30% year to date. Although it is just over a tenth the size of the European market, the Middle East and Africa grew rapidly, up 62% year over year to lift the EMEA region’s growth to above 32% in GWh terms.

In absolute terms over the four months, EV buyers in the Asia Pacific region rolled 176.8 GWh of fresh battery capacity onto the region’s roads while European drivers (including those in the UK, Russia and non-EU states) added 63.5 GWh and those in the Americas 45.0 GWh. The Middle East and Africa’s contribution of 6.4 GWh to global battery capacity deployment now translates to more than 2% of the total.

BEV buying beefed up

The strong start to the year in Europe was due in part to a change in the sales mix towards full electric vehicles with BEV sales rising by 27% year to date compared to a less than 12% expansion for new plug-in hybrid registrations.

In Asia Pacific, BEVs have also outpaced PHEV sales so far in 2025, reversing a trend in place for the last few years. BEVs represented just under half of the five million electrified vehicles sold in the region from January through April this year, led by China where 55% of EV buyers opted for full electric vehicles.

In contrast, in Japan, the second largest market in the region drivers opted for conventional hybrids nine times out of ten while BEV and PHEV registration pulled back sharply compared to the same period in 2024.

The same trend can be seen in the US. BEV sales in the country make up only around a third of the total after growing by 9% year on year compared to HEVs which found 37% more buyers in 2025. The minimally electrified conventional hybrids now constitute 56% of the American EV market.

Bumps in the road

The US budget bill now before the Senate may water down some of the provisions approved by lawmakers cutting back on EV subsidies and incentives, but coming on the back of already disruptive tariffs, the North American electric car market could struggle to regain momentum this year.

It’s not only the US where clouds are hanging over the EV industry. Last week, Beijing called in 16 domestic carmakers to discuss worrying trends on the market, where years of cutthroat competition have put immense financial pressure on many if not most players.

Observers believe it is only a matter of time before the race to the bottom will result in bankruptcies along the EV supply chain and likely a weeding out of less competitive smaller OEMs.

The impact on the consumer remains to be seen – Chinese car buyers are spoilt for choice with nearly 100 competing EV brands and thousands of models and variants that cater to every conceivable demographic.

Government support remains in place and a stronger if less diverse electric car industry should mean China will be leading global vehicle electrification for a long time to come.

Contact the Adamas team to learn more or check out the intelligence services below.