Top 5 global EV cell suppliers by battery capacity deployed

In 2024, 864.0 GWh of battery capacity were deployed onto roads globally in all newly sold passenger EVs combined (including plug-in, range extender and conventional hybrids), up 25% over calendar 2023.

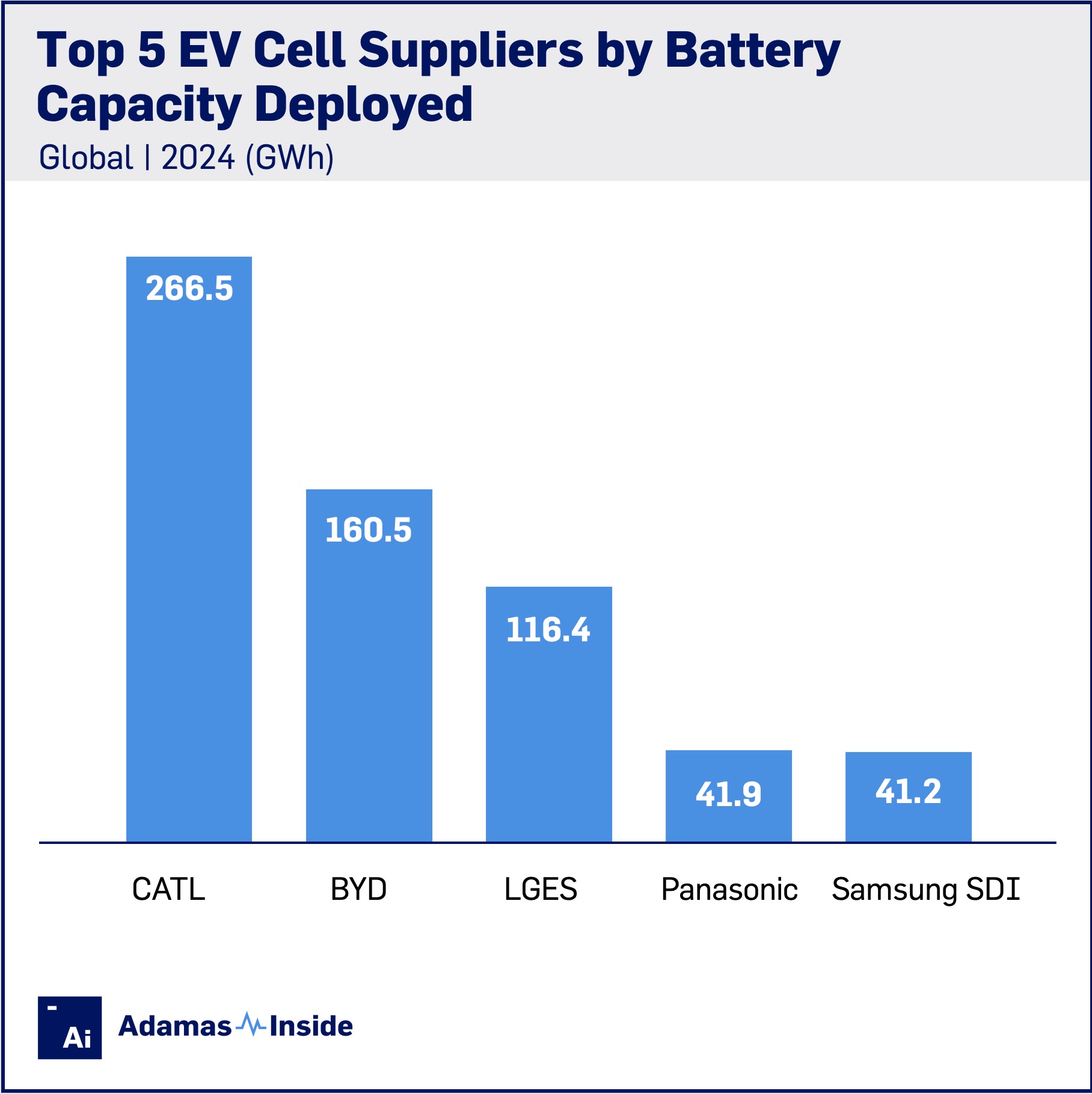

Among EV cell suppliers, CATL led the pack with 266.5 GWh of combined battery capacity deployed worldwide 2024, a 24% jump compared to the year before. The Chinese battery giant cornered 31% of the global market in GWh terms last year, down a fraction compared to 2023.

In a distant second place for the calendar year was BYD at 160.5 GWh. BYD, the number one EV maker globally which now sells an all-LFP battery powered fleet, added an eye-catching 40% more battery capacity to the world’s highways and byways last year increasing its share of the total to 19% from 17% in 2023.

The combined capacity of all EVs sold last year fitted with a battery manufactured by LG Energy Solution declined by 4% year on year hitting 116.4 GWh in 2024. Ultium Cells, a General Motors joint venture with LG Energy Solution, falls just outside the top 10, but the US firm recorded an eight-fold increase in deployment to 18.5 GWh.

Among the top tier EV cell suppliers Panasonic had the most difficult year with its performance in GWh terms dropping 22% compared to 2023. Panasonic built its EV battery business through a long running partnership with Tesla in the US but as the automaker’s production shifted to China with CATL as supplier, the Japanese company struggled to keep momentum.

Nickel metal hydride batteries used in conventional hybrids, where average battery size seldom exceeds 2 kWh, made up 10% of Panasonic’s business last year after a 12% year on year expansion, but the overall capacity of the third generation NCA cells supplied to Tesla shrank by 35% in 2024 over 2023.

Rounding out the top five was Samsung SDI, which is now within a stone’s throw of Panasonic after deploying 41.2 GWh in 2024, a 6% increase. Samsung’s top customer is BMW, which had an exceptional 2024: nickel-rich batteries supplied to the German marque jumped 36% in GWh terms.

EV cell manufacturing remains a top-heavy affair with the top five firms responsible for 73% of the combined battery capacity deployed on the world’s highways and byways in 2024, although that figure is down from 78% in 2023.