CHART: How nickel, cobalt and manganese are being squeezed in the global battery metal basket

Last year was a record year for the global EV market by unit sales, battery capacity deployment and metals consumption.

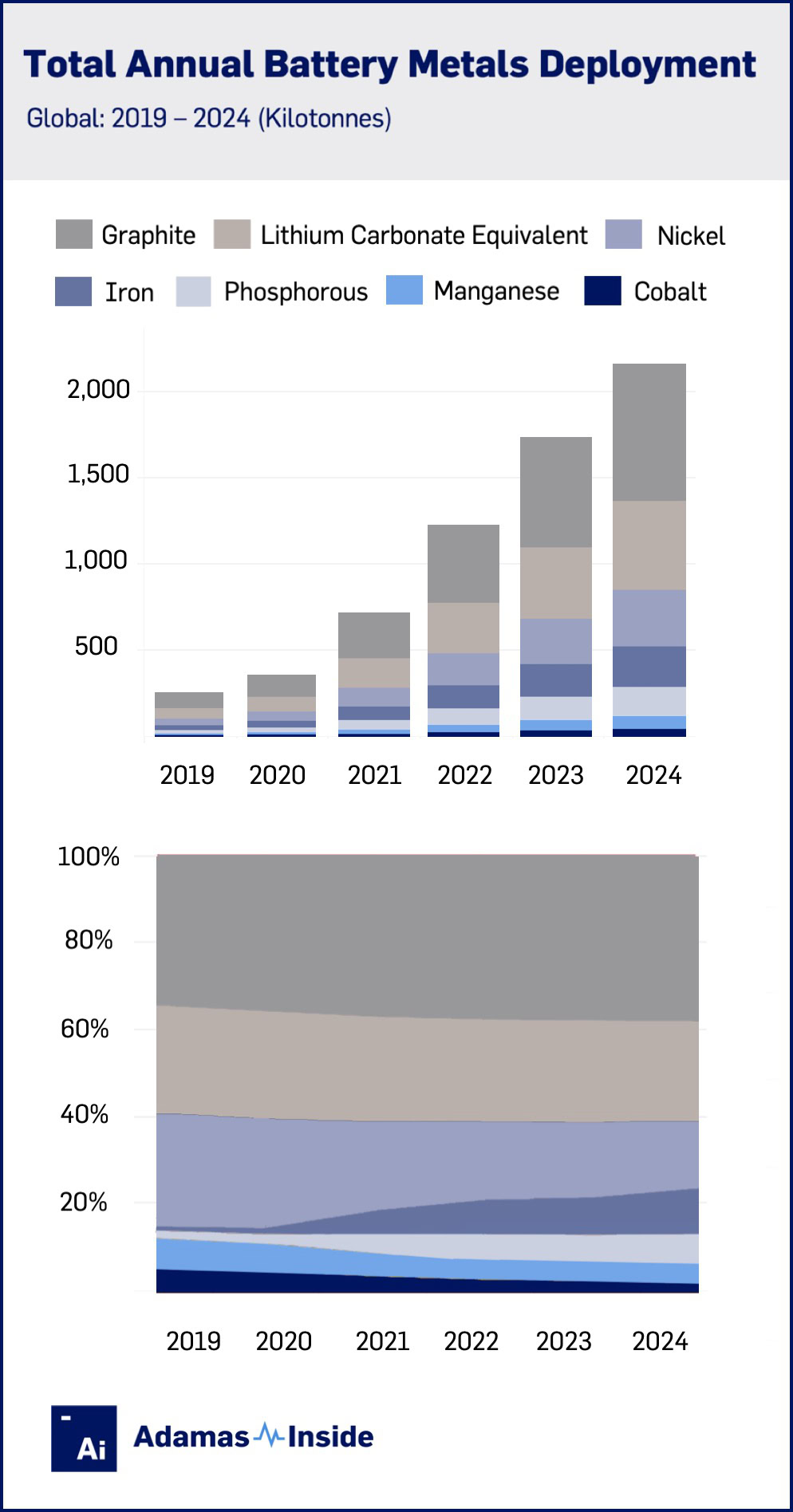

In 2024, a total of 2.2 million tonnes of graphite, lithium, nickel, iron, phosphorous, manganese and cobalt were deployed onto roads worldwide in the batteries of all newly-sold EVs combined, including plug-in and conventional hybrid electric vehicles.

At 26% year on year growth, battery metals consumption slightly outpaced the 25% expansion in GWhs deployed, which hit 865.5 GWh in 2024.

Another breakout year for Chinese automakers, including top EV maker BYD with its all-LFP line up, boosted LFP’s share of the global cathode mix to 40% last year, and its share in China to 58%, on a GWh deployed basis.

The China-fueled rise of LFP has fostered a large divergence in global consumption growth rates of key battery metals.

For example, iron and phosphorous deployment were up by 54% and 49%, respectively, last year for a combined 399.1 kilotonnes (kt) rolled onto roads over the course of 2024.

In contrast, global nickel deployment into EV batteries increased just 11% to 322.7 kt while that of manganese rose 10% to 73.6 kt and cobalt 7% to 59.6 kt as the industry continues to thrift the costliest of the battery metals.

In total, installed tonnage of nickel, cobalt and manganese last year represented 21% of the battery metal basket. That’s down from a 24% share in 2023 and 36% in 2020 when BYD’s so-called Blade battery and LFP-powered Model 3s re-ignited the rise of the Ni-Co-Mn-free battery chemistry.

For suppliers of these metals to the EV industry, the less than positive deployment trend since 2020 has been made worse by falling prices.

According to Adamas analysis, the value of battery nickel deployed onto roads last year declined by 5% year on year to $5.7 billion while that of cobalt fell nearly 20% to $1.2 billion. Manganese was the silver lining with a 9% rise to $179 million.

In 2025, there is little reason to believe that LFP’s march in China will be slowed. Overseas, however, LFP factory buildouts in the Americas and Europe, where LFP packs only constituted 10% of the market last year, has been slow albeit several large projects are expected to enter production in the next few years.

Until then, cobalt and manganese deployment will receive some support from the continued popularity of mid-nickel cathodes in China, which contain two- to three-times the cobalt and manganese of high-nickel cathodes. The latter’s demand will also continue to be propelled higher by the ongoing roll-out of LMFP batteries.

From a standing start, Adamas data shows that 3.1 GWh of LMFP were deployed onto roads in newly-sold EVs last year.

LMFP is set to eat into the market share of conventional LFP over the coming years but arguably presents less of a threat to NCM chemistries.

Contact the Adamas team to learn more, or check out the intelligence services below.