The 10 GWh Club: Ranking the world’s top electrified vehicle manufacturers

Calendar 2024 was a record-breaking year for the global electric vehicle industry. In total, 865.5 GWh was added to the electric car parc, an expansion of 171.8 GWh or 25% compared to the year before.

Nearly a third of all passenger EV battery capacity deployed (including plug-in and conventional hybrids) since the emergence of the industry were rolled onto roads last year alone.

Swings and roundabouts

There are more than 70 auto manufacturers making electric cars around the world and still more brands. Most of them are Chinese and many with monikers few may have heard of outside their home market: Trumpchi, Cao Cao, Lingbox, Jetour, Hongqi, Skywell, Huazi Ohmycar, Jemell, Aeolus, and Sehol to name a few.

China’s crowded EV market is in the midst of a brutal price war and the race to the bottom has been relentless.

Rinky dinky micro-cars like the Chery QQ Ice Cream and perennial bestseller the Wuling Hongguang MINI can now be had for the equivalent of $5,000 or even less.

The far from bare bones BYD Seagull still retails for under $10,000 in China even after an upgrade to “God’s Eye”, the EV maker’s advanced driving assistance system.

In the luxury and sports segment, prices are similarly mouth-watering for tire kickers, and profit margins equally razor thin for automakers.

The Xiaomi SU7 introduced in China in the second quarter of last year starts at the equivalent of $42,0000 and tops out at around $75,000 for the track racing variant. The Porsche Taycan by comparison starts at $95,000 and with options go all the way up $250,000.

Speed to market

While cutthroat competition in the Middle Kingdom will see more makes fall by the wayside, Chinese automakers’ fondness for creating spin-offs to cater to every possible segment and demographic (Geely, Chery, Dongfeng and even BYD are particularly guilty) saw some roaring successes.

Chinese EV makers expanding into more upmarket segments, adding large SUVs and MPVs to model line-ups, and those riding the PHEV and EREV wave, had an exceptional year – with exceptions.

The once high-flying HiPhi startup shut its doors in August. Owners Human Horizons, founded by a former exec of Ford and General Motors in China, only launched its HiPhi Z sedan in 2022 but with prices starting at $80,000, staying in business was always going to be an uphill climb.

While failures in a nascent industry are to be expected, last year also saw the highly successful introduction of new brands with owners emanating from the tech and telecoms industry, treading where US tech giants feared to rush in.

Show me how it’s done

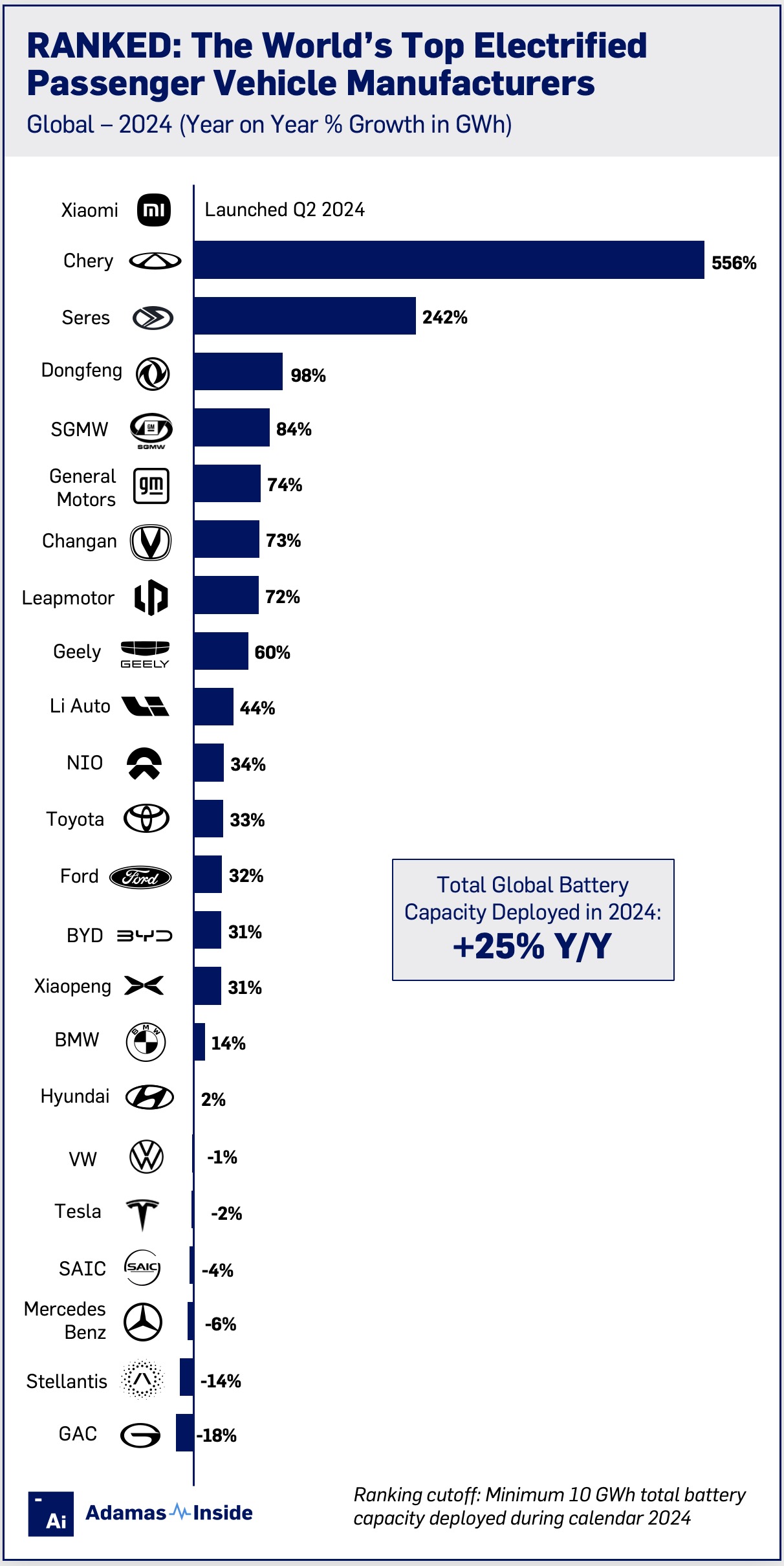

From a standing start Xioami’s SU7 rolled enough power hours onto Chinese roads last year to buy the mobile phone maker entry into the 10 GWh club.

While Xiaomi used a contract manufacturer – the state-owned BAIC Group – to get motoring quickly, the company’s own highly-automated factory outside Beijing is now operational with claims that the plant can churn out 40 cars per hour on a single assembly line.

At the start of 2025, the SU7 overtook Tesla’s Model 3 to become the second-most popular in the world after the Model Y despite being only available in China.

It was only the second time since entering full production that the Tesla workhorses did not occupy the top two slots in any given month globally (the only other occasion being September 2023, when BYD’s Yuan Plus/Atto 3 briefly had the honor).

Given its debut for the ages last year, Xiaomi’s YU7 SUV – a direct competitor to the Model Y – launching this year may well vie for the EV world’s top spot.

Cherished luxury

The Luxeed R7 is a coproduction by Huawei and Chery and helped the automaker, associated more with runabouts like the aforementioned QQ Ice Cream, catapult into position 12 in the ranking from an also ran in 2023.

Only launched in October, the R7 mid-size EREV crossover was the fourth most popular model globally in January – already in the slipstream of the Model 3 after proud new owners rolled more than 1.0 GWh onto roads in a single month.

The combined battery capacity of EVs in the Chery stable sold last year, which also includes the Exeed, iCar and Jetour brands, amounted to 20.5 GWh, a 17.3 GWh or 556% surge from 2023.

This year Chery is targeting Europe with its Jaecoo and Omoda badges, while the high-end Exlantix moniker is already being sold in Russia. Chery was founded in 1997 and to this day is wholly owned by the Wuhu municipality in Anhui province China.

The Seres Group had a phenomenal year supplying 242% or 12.0 GWh more pack power to buyers of its eponymous and Aito brands. Known as Wènjiè in China, Aito (Adding Intelligence to Auto), is another luxury vehicle and Huawei tech partnership success story of 2024.

Its top seller, the Aito M7, also caught China’s EREV wave and the cross-over accounted for nearly half of Seres Group GWh deployed last year. Despite having on average substantially smaller batteries than full electric vehicles, the market for extended range vehicles where the combustion engine acts solely as a generator, expanded by 93% in GWh terms last year.

Nippon nibbles

Out of the 23 EV makers (five more than in 2023) that deployed 10 GWh or more total battery capacity in 2024, 14 are Chinese while the ranking only features a single Japanese entry, Toyota.

Toyota expanded battery capacity deployed by a third year over year. However, the world’s largest automaker’s heavy reliance on conventional hybrids which accounted for nine out of every 10 passenger electrified vehicles the Japanese company shipped last year, saw drivers of new Corollas, Camrys and RAV 4s add just 17.6 GWh to global roads. Toyota slipped from number 13 to sixteenth in 2024.

The same reliance on HEVs is at work at Honda. Honda is ranked 29th with 6.2 GWh deployed in 2024 despite a 172% jump in its fleet electrification efforts. Honda’s eye-catching 0 series of BEVs to be assembled at its Ohio facilities will only go on sale in 2026.

At Nissan HEVs accounted for 76% of sales last year, ranking the company ahead of Honda at 26th after a lukewarm 5% growth. Even with a new CEO announced in Mach, Nissan’s problems run much deeper than a sluggish EV strategy.

And finding a white knight in Honda, or Chinese contract manufacturer Foxconn which had long pursued the Japanese firm, appears to be a dimming prospect.

BYD dreams

BYD surpassed Tesla in sales earlier but 2024 was the first calendar year where the Shenzen-based company beat the US EV pioneer on a GWh basis.

Tesla and BYD crossed the 100 GWh mark in 2023, but BYD closed the gap considerably last year deploying 31% or 33.9 GWh more in 2024 thanks in no small part to its extensive PHEV portfolio.

Buyers of BYD’s Denza vehicles added nearly double the power hours to Chinese roads in 2024 than the year before and the upmarket Yangwang marque achieved 274% growth but together these brands still make up less than 4% of their parent’s deployment.

BYD EVs sold in Europe and the Americas make up less than 5% of its tireprint and Brazil is by far its largest export market. The South American nation implemented its own set of EV tariffs well before the EU and BYD is now building a large plant there.

BYD raised $5.6 billion in Hong Kong’s largest share offering in four years at the beginning of March, to be used mainly for its overseas expansion which, given tariffs and other obstacles outside Asia, is expectedly slow.

In January the BYD Shenzhen undocked for the first time. The roll-on roll-of (RoRo) vessel is the world’s largest with space for 9,200 vehicles – yet another sign that the company’s global ambitions remain undiminished.

A fork in the road

Tesla was one of six automakers recording a year on year decline albeit a modest 2% or 1.9 GWh to 129.9 GWh, led by the Model Y, the bestselling passenger vehicle of any kind globally last year.

Tesla’s mid-size SUV contributed 10% to the world’s car parc electrification at 85.6 GWh with the Model 3 sedan adding another 35.0 GWh.

Tesla’s prospects for 2025 are murky. Political protests in the US and Germany against CEO Elon Musk are likely to continue and Tesla’s sales plunge in some markets at the opening months of 2025 may not bounce back.

After its first full year on sale, the controversial Cybertruck could struggle to find new converts although in 2024 the beefy pickup contributed only 4% of Tesla’s overall battery capacity deployed.

Conversely, Tesla’s weak sales at the start of 2025 can at least partly be blamed on customers holding out for the new Model Y coupled with lack of supply as the company ran down inventories.

The long-awaited ‘Juniper’ refresh has been well received including in China where orders have already started. The Model Y also occupied the top spot in the world’s largest EV market in 2024 and a new budget version of the SUV for the Chinese market is said to be in the works.

Then there’s the on-again, off-again sub-$30,000 car (dubbed the Model Q or 2 among speculators) which Tesla execs in the company’s 2024 results call said is on track for launch in the first half of 2025.

US manufacturers Ford and General Motors outperformed in 2024, upping battery capacity deployed by 32% to 17.0 GWh and 74% to 21.0 GWh respectively last year. GM cracked the top 10 for the first time with the Chevrolet Equinox, Blazer and Cadillac Lyriq doing most of the heavy lifting.

In the US, Ford’s F-150 Lightning and Mustang Mach-E was placed third and fourth, followed by the Cybertruck.

European easing

Among the losers, the vast Stellantis stable – Chrysler, Dodge, Jeep, Ram, Fiat, Alfa Romeo, Maserati Folgore, Peugeot, Citroën, DS, Opel, Vauxhall, Abarth – had a dismal year declining by a combined 14% in GWh terms.

Other Europe-based companies followed Amsterdam-headquartered Stellantis down the wrong path. No 4 Volkswagen experienced a 1% in decline battery capacity deployed to 59.6 GWh.

Wolfsburg’s performance may have been worse was it not for the 20% gain for its VW-badged EVs sold in China by partner SAIC and a solid 14% improvement for Porsche, where deployment grew by 14% to a 4.5 GWh in 2024.

For Mercedes-Benz it was a steeper 6% fall to 20.6 GWh, while its nearest rival BMW, including MINI and Rolls Royce, achieved double-digit percentage growth year-on-year lifting the Munich-based company to fifth place at 34.8 GWh, overtaking Hyundai-Kia which only managed a 2% expansion.

While its German peers are recalibrating their EV strategies, BMW declared a ‘tipping point’ for the internal combustion engine back in January 2024 and new models following its radical design overhaul – the Neue Klasse – will start production later this year.

Huawei or the highway

GAC Group which sells Trumpchi and Aion EVs was the worst performer among the top tier, down by 18% or just shy of 6.0 GWh. Trumpchi, which focuses more on PHEV and HEVs, had a great year increasing battery deployment by 186% but makes up less than 2% of the group’s battery capacity deployment.

State owned vehicle manufacturer Guangzhou Automobile Group’s EV brand was established in 2017 and the firm also manufactures EVs on behalf of Honda and Toyota in China.

In 2021 GAC and Huawei signed a deal to jointly develop an electric SUV, but the arrangement was terminated less than two years later.

Likely cognizant of the success of Chery and Seres, the two companies revived their partnership in November last year to create an all new BEV brand competing in the same upmarket segment as Luxeed and Aito. The first model should roll off assembly lines in 2026. And prove whether lightning can strike thrice.

Contact the Adamas team to learn more or check out the intelligence services below.