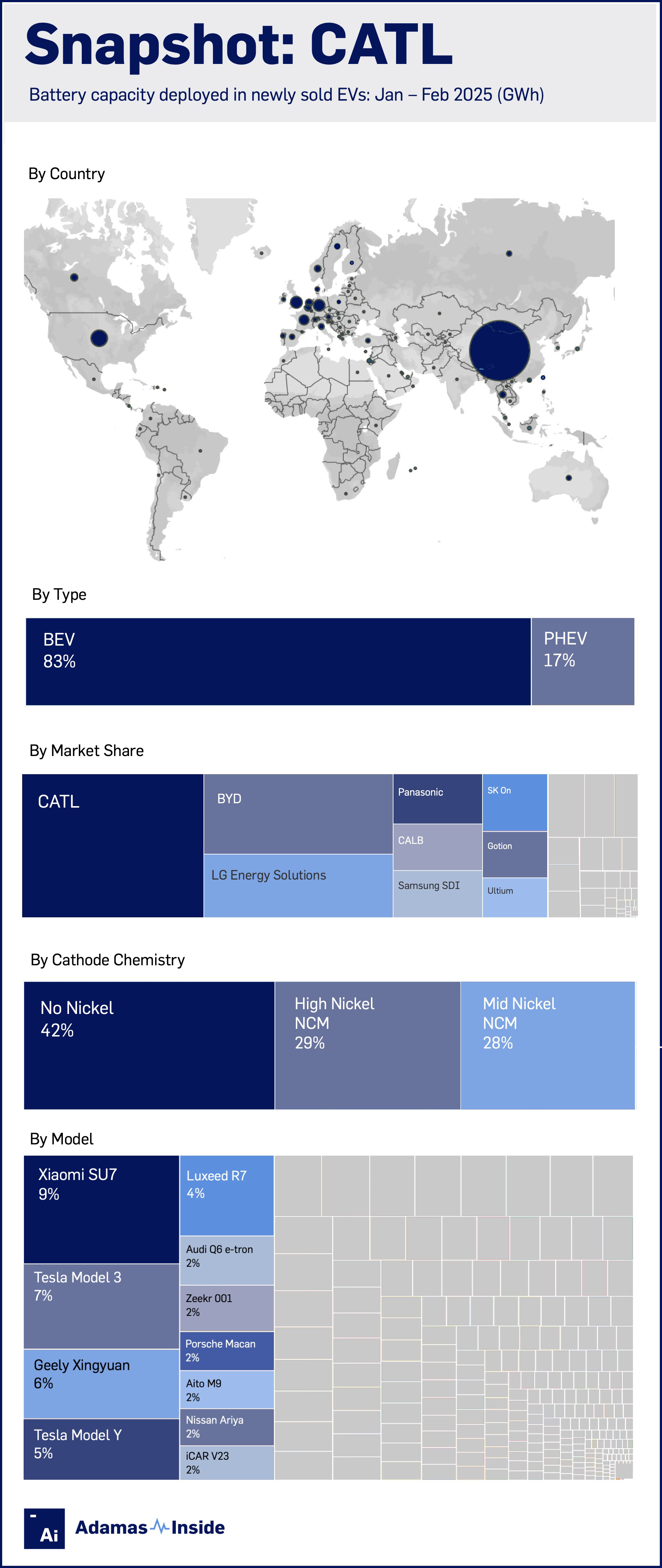

Snapshot: CATL – the global EV battery hegemon

Contemporary Amperex Technology Co, the global EV battery leader by a country mile, is not sitting on its laurels.

Last month, at its so-called Tech Day in Shanghai, the company widely referred to as CATL, announced three EV battery breakthroughs.

CATL’s second-generation Shenxing LFP packs promise significantly faster charging while the company claims the energy density of its novel Naxtra sodium-ion batteries overcomes the inherent limitations of the chemistry, making it suitable for the EV market.

CATL also unveiled the attention grabbing Freevoy Dual-Power battery that combines two chemistries (details of which the company is keeping close to its chest) that is said to achieve 1,500 km or 932 miles of range in full-electric vehicles.

And as has become expected from China’s EV market leaders, the new tech is not hitting the streets on some vague future date. CATL is bringing sodium-ion batteries into commercial production as soon as the end of this year, while the first BEVs with dual-power packs could roll out of showrooms as early as 2027.

GWh giant

CATL is based in Ningde, Fujian Province, and in its current form traces its founding back a mere 14 years which makes its dominance of the global EV battery market all the more impressive.

According to data from the Adamas EV Battery Intel Platform, through the first two months of 2025 CATL cornered 30% of the global market by battery capacity (GWh) deployed onto roads in newly sold passenger EVs.

At 37.2 GWh deployed, the company has a healthy (albeit slightly narrowing) gap to top EV maker BYD, itself a prolific battery technology innovator. CATL grew by 25% in January-February 2025 compared to BYD which is off to the races this year recording a 41% jump.

CATL’s client base runs the gamut of automakers including China’s Changan, Chery and Geely and their many brands, BMW, Volkswagen, Mercedes-Benz, Stellantis and a host of other Western marques, and Japanese and Korean EV brands.

CATL batteries also make it into Xiaomi vehicles – the Chinese mobile phone maker’s entry into automaking has been a runaway success and its SU7 sedan is now the top CATL-powered vehicle globally, displacing the Tesla Model Y.

CATL and BYD together with Korea’s LGES – the Battery Big 3 – control over 60% of the market – more evidence of the benefits of economies of scale in a rapidly growing and competitive industry that supports more than 60 players.

Over the last decade, CATL has contributed over 800 GWh to the electrification of the global car parc and is on course this year to become the first EV battery maker to pass the TWh milestone.

Tesla remains CATL’s top customer and on a cumulative basis nearly a fifth of the company’s battery capacity deployed hit the streets in Tesla models.

BYD has moved to an all LFP model lineup and CATL’s business is also increasingly being built on no-nickel cathode chemistries.

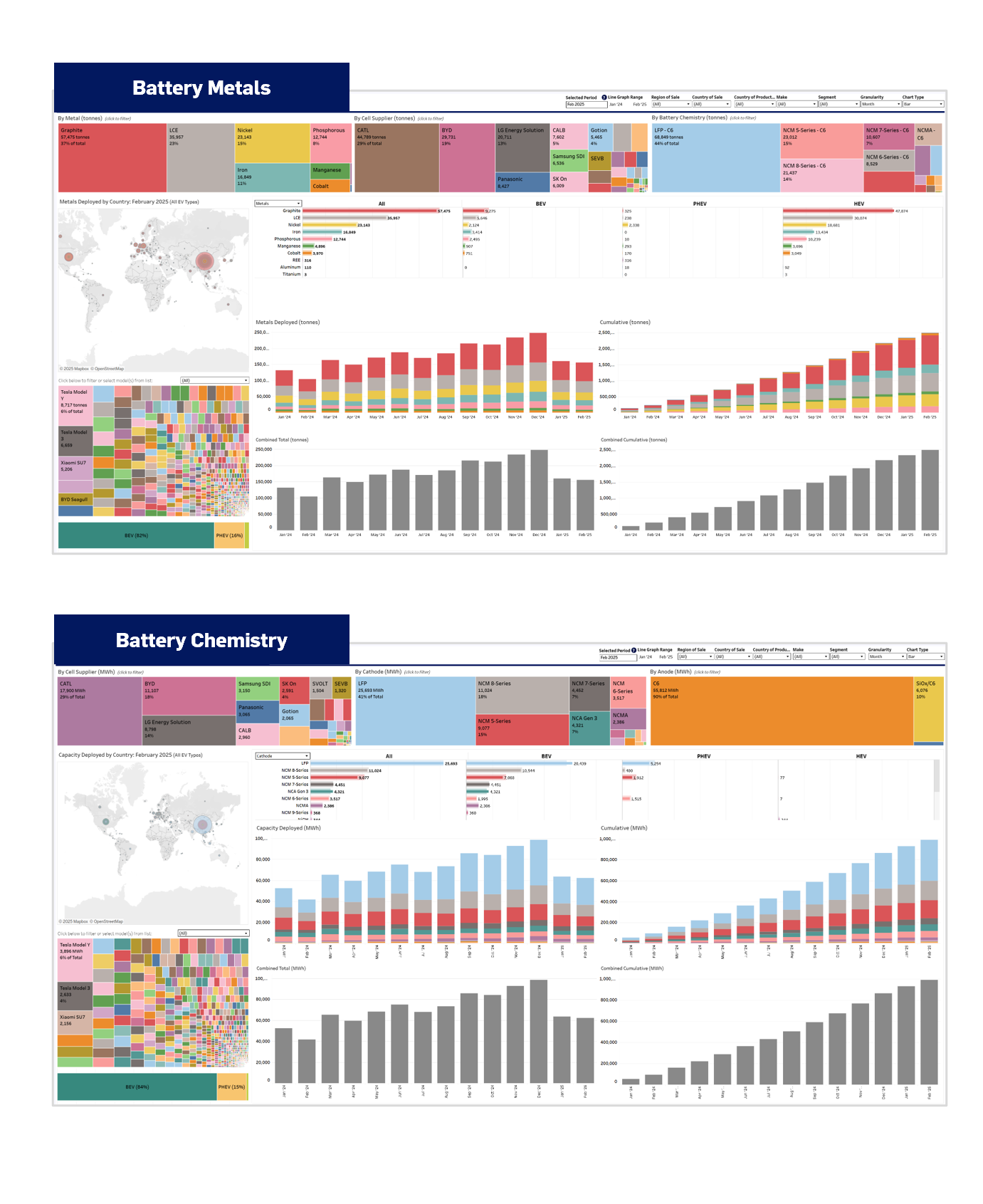

EV Battery Intel Platform

The most detailed market data on EVs, batteries, metals and suppliers

LFP expansion

EVs powered by CATL’s LFP packs rolled 63% more GWh onto the world’s roads during January and February compared to the same months last year, while LMFP deployment grew by a factor of seven.

During that same time the company’s mid-nickel batteries deployed shrunk by 7% while its high-nickel packs added 10.9 GWh to the world’s highways and byways, 26% more than last year.

CATL has found expansion outside of China slow going and the company relies on the Asia Pacific for 76% of its capacity deployment. In China, LFP represented 65% of battery capacity deployed in January and February.

The presence of CATL, and LFP, in Europe is set to rise rapidly however.

CATL’s largest operating plant outside China is in Thuringia, Germany. A giant 100 GWh factory currently under construction in Debrecen, Hungary is set to come on line later this year, and plans for a 50 GWh facility in Zaragoza, Spain are far advanced. All three manufacture LFP cells.

Currently, CATL’s penetration in GWh terms in the Americas is a shade under 7%.

Ford’s 20 GWh LFP plant under construction in Michigan is slated to be commissioned next year with the US automaker initially announcing that it would be licensing CATL’s LFP technology. But given the trade and political tensions between the US and China, the nature and extent of CATL’s involvement remains unclear. Ford has teamed up with Korea’s SK On for factories in Tennessee and Kentucky.

Tesla is also rumored to be working with CATL on facilities including for stationary energy storage in Nevada and Texas given the two EV leaders’ long relationship, but as with Ford political sensitivities limit the Chinese company’s investment in the region and details remain scarce.