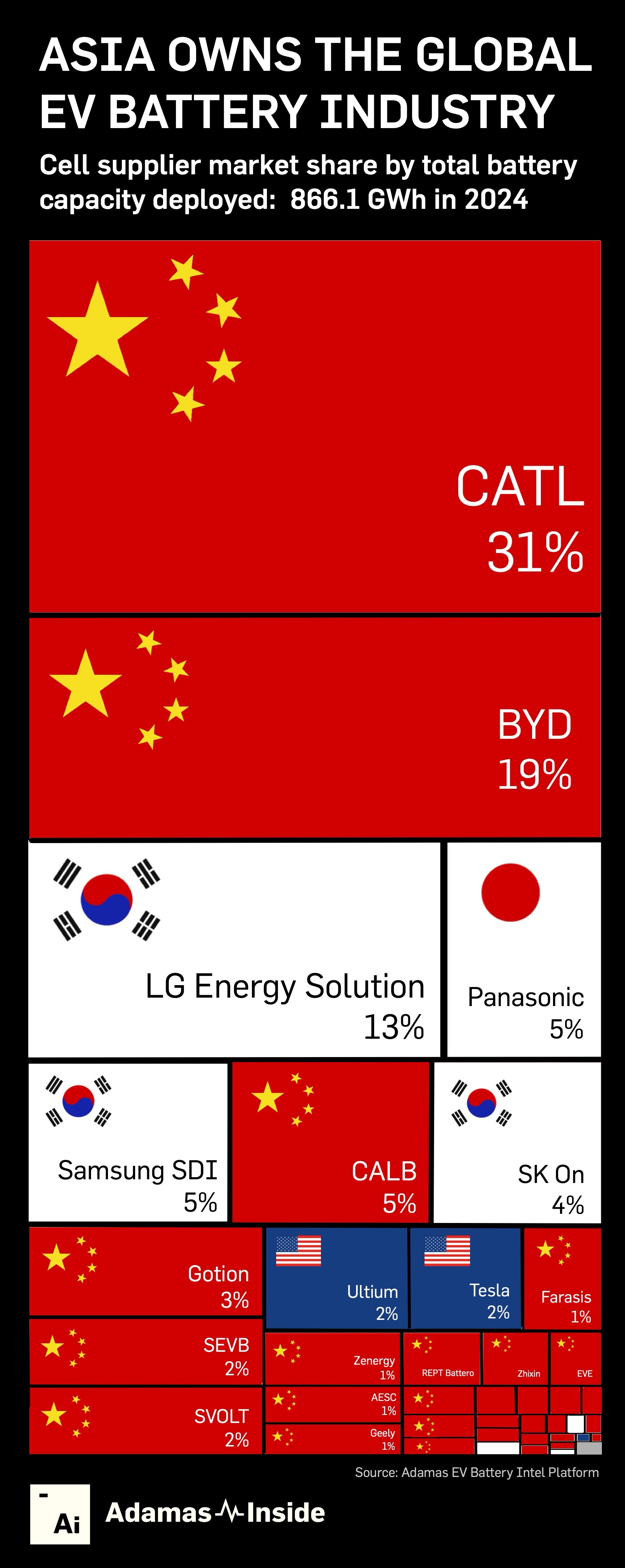

CHART: Asian cell suppliers’ dominance of the EV battery market

During the first two months of 2025, 126.0 GWh of battery capacity was deployed onto roads globally in all newly sold passenger EVs combined, 34% more than the same period last year.

The Asia Pacific region expanded at a faster pace than the rest of the world (+38%) even though the region already represented more than 60% of global market in GWh terms going into 2025.

Given that China itself represents over half of global EV battery capacity deployment and to smooth out the effect of the lunar holiday which fell early this year, Adamas aggregated deployment data for January and February to make meaningful year-on-year comparisons.

EV battery manufacturers and cell suppliers based in China, South Korea and Japan have almost complete control of the global market. The accompanying graph shows the market share of cell suppliers by country of ownership in calendar 2024 when a record 866.1 GWh of battery capacity was deployed worldwide in EVs sold during the year.

January and February data extracted from the Adamas Battery Intel Platform shows only minimal changes to the dominance of Asian cell suppliers so far this year.

Contemporary Amperex Technology Co Limited or CATL, long the clear industry leader, saw its global market share in GWh terms dip to just below 30% at 37.2 GWh, hurt by declining shipments by its top customer Tesla during the opening months of the year.

CATL’s client base runs the gamut of automakers including China’s Changan, Chery and Geely and their many brands to BMW, Volkswagen, Mercedes-Benz, Stellantis and a host of other Western marques.

The Fujian province-based company’s plans to take on the European market are ambitious – CATL’s largest operating plant outside China is in Thuringia, Germany, a giant 100 GWh factory is currently under construction in Debrecen, Hungary, and plans for a 50 GWh facility in Zaragoza, Spain are far advanced.

CATL batteries also make it into Xiaomi vehicles – the Chinese mobile phone maker’s entry into automaking has been a runaway success and its SU7 sedan is now the top CATL-powered vehicle globally, displacing the Tesla Model Y.

The combined capacity of BYD packs rolled onto global roads during the first two months of the year outpaced the overall market growing by 41% to 21.6 GWh.

LG Energy Solution, the South Korean member of the Big 3 which combined have cornered 60% of the global market, saw 29% more GWh hit roads in EVs equipped with its batteries.

With the notable exception of Panasonic (–8% to 6.3 GWh and also a victim of weak Tesla deliveries) and Samsung SDI, which saw deployment decline by 4% to 5.9 GWh during the period, cell suppliers further down the ranking had great success in 2025.

China’s CALB increased battery capacity deployed by 55% year over year to 6.0 GWh, overtaking its Korean rival, which held the fifth spot for 2024. CALB’s Chinese peers, Gotion, at number eight, and SVOLT, placed 10th, also handily beat the market this year, raising deployment by 65% and 70% respectively in January-February. Korea’s SK On, placed seventh, lost market share, but still managed to increase deployment by a healthy 23% to 5.4 GWh.

The standout performer year to date is Ultium Cells, a partnership between GM and LGES, which increased battery capacity deployment in newly-sold EVs by 371% in January and February versus the same two months in 2024 hitting a total of 3.7 GWh.

The total capacity of batteries deployed at Tesla’s global headquarters in Austin during the two-month period jumped 50% year on year to 2.1 GWh.

Overall, North American cell suppliers garnered slightly less than 5% of the global market (up from 4% in 2024).

Cell suppliers outside the top 10 together deployed 15.1 GWh during the first two months, a 60% increase over 2024.

Adamas tracks over 60 companies supplying EV cells worldwide, the vast majority in China. A maturing EV industry is likely to become less top-heavy over the coming years.

However, as the $8 billion failure of Europe’s great battery hope – Northvolt – has shown, the benefits of economies of scale and institutional knowledge of the still fast-growing EV industry cannot be underestimated.

Moreover, without the battery metal supply chain which, China also dominates, creating alternative cell providers outside Asia will remain a tall order.

Contact the Adamas team to learn more or check out the intelligence services below.