Manganese malaise: Loading in average EV battery down 14% year-over-year

Despite the rosy outlook for manganese use in next generation EV batteries, including lithium-manganese-iron-phosphate (LMFP), lithium-manganese-nickel-oxide (LMNO) and other nickel-manganese (NMx) based cathodes, our latest quarterly deployment data suggests that manganese use in the average passenger EV battery is trending down.

The Adamas Intelligence Battery Metals Intel Platform shows average manganese mass in passenger EV batteries, including plug-in and conventional hybrids, was down 14% year-over-year in the third quarter to 3.1 kilograms.

By EV type, the average BEV’s manganese loading dropped by 14% year-over-year in Q3 to 4.9 kilograms. Over the same period, the average PHEV’s manganese content fell 7% (despite a 6% expansion in average battery capacity) and that of the average HEV went unchanged.

Nickel ascent

While much of the lost ground for manganese can be ascribed to the massive adoption of LFP batteries, particularly in China, the move to high nickel batteries with reduced manganese and cobalt contents is also playing a role.

Early NCM cells used nickel-cobalt-manganese in a roughly 1:1:1 ratio, but now this mix commands less than 1% of the EV market in terms of GWh deployed globally.

The NCM cathode of choice in Q3 2024 has a ~5:2:3 split of these metals and captured 18% of the overall market in Q3 2024 by GWh deployed.

While Chinese automakers still rely on the NCM 5-Series for many of their mid-tier offerings, Adamas data shows that the cathode is not as widely used elsewhere, representing less than 1% of the quarter’s overall battery capacity deployment in the Americas, and less than 5% in Europe where NCM 8-Series is dominant.

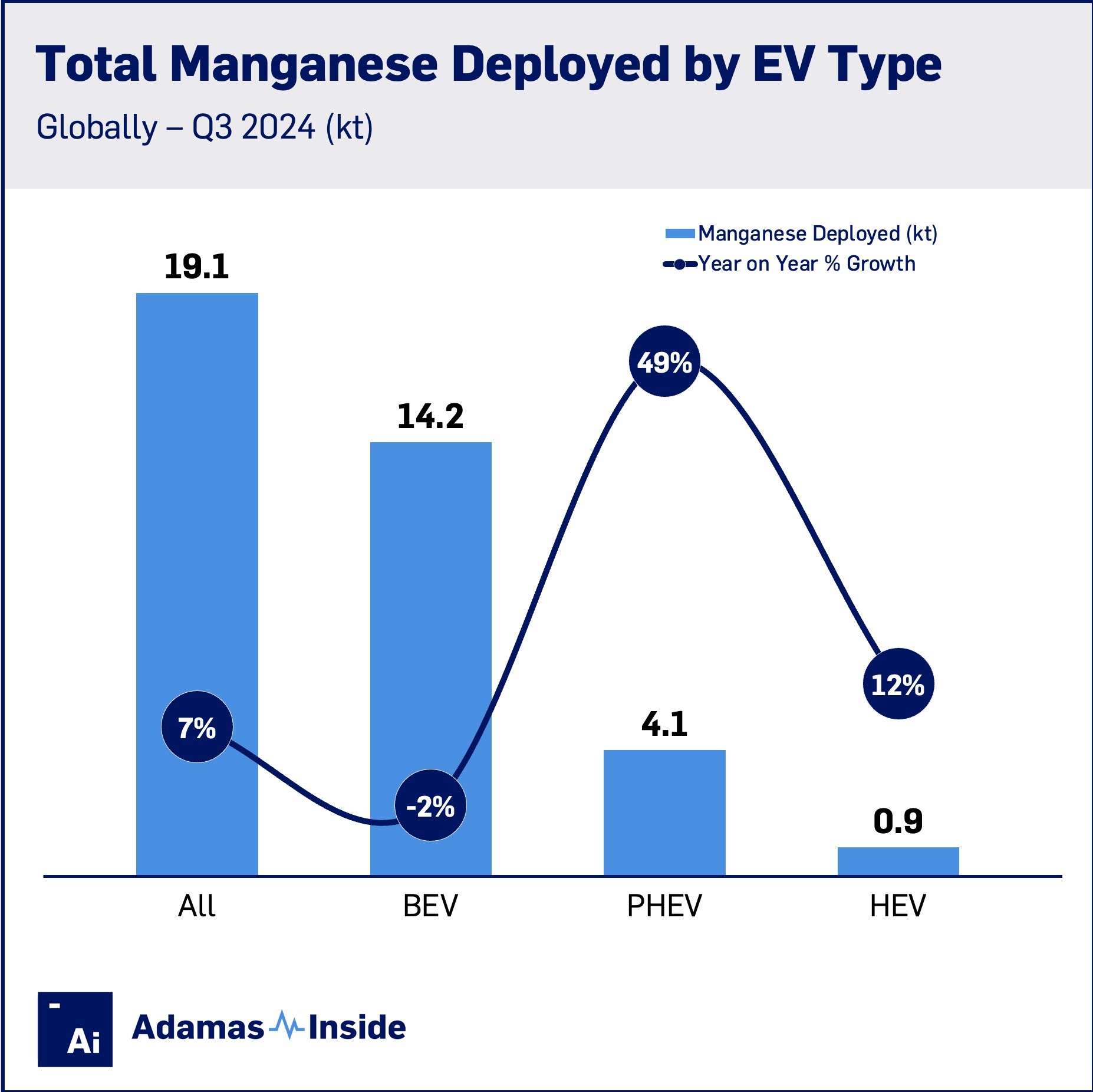

Nevertheless, despite manganese loading per average EV trending down overall, total manganese deployment in all EVs combined increased 7% globally in Q3 2024 to 19,100 tonnes.

During the quarter, manganese deployment in BEVs fell 2% versus the same quarter the year prior while deployment into PHEV batteries jumped 49% and HEV batteries 12%, collectively offsetting weakness in the BEV market.

LMFP exceeds

An encouraging observation for manganese suppliers is the runaway success of the Luxeed S7 (shown in picture), the Huawei-Chery JV’s flagship sports sedan which comes fitted with a beefy LMFP pack manufactured by CATL.

Despite only being introduced in Q1 of this year, LMFP was already responsible for 2% of global manganese deployment onto roads in Q3, largely in the packs of the aforementioned S7.

Other cell suppliers investing in LMFP manufacturing capacity include BYD (which today has an all-LFP model line-up), Gotion and SVOLT. Tesla has reportedly validated its use in vehicles made in China with cells from its long-term supplier in the country, CATL.

With around 15–20% higher energy density than LFP and purported better cold weather performance, LMFP is set to eat into the market share of conventional LFP over the coming years, but arguably presents less of a threat to NCM chemistries.

After years of LFP market share growth chiseling into manganese, rising adoption of LMFP batteries (and other Mn-rich cathode chemistries) is poised to turn the tide for producers of the metal.

—

Methodology: We analyze the battery specifications, battery chemistries, and metal loadings of every unique passenger EV model-version (e.g., 2024 Tesla Model 3 Performance AWD (MIC) – 4th generation) produced and sold globally each month with historical data back to January 2004 (~3,000 model-versions).

With this industry-leading granular insight in hand, we track global monthly production, trade and sales of each model-version for over 180 automakers in over 110 countries to accurately assess the competitive landscapes of cell suppliers and cell chemistries, and to quantify battery capacity and battery materials deployment onto roads, from the bottom up.

Reported battery capacity and materials deployment constitute installed terminal watt-hours and/or tonnes of materials and do not take into account losses during conversion, refining and manufacturing processes.

Contact the Adamas team to learn more or check out the intelligence services below.