High Nickel Cathodes Dominated the Passenger EV Market in 2020

High Nickel Cells Made Up Over 60% of Passenger EV Battery Capacity Deployed Globally in 2020

In 2020, a total of 134.5 GWh of passenger EV battery capacity was deployed onto roads in new BEVs, PHEVs and HEVs sold globally, as we examined in a recent insight.

Over 60% of all passenger EV battery capacity deployed globally in 2020 was in the form of high nickel cells, such as NCA or NCM 6- to 8-Series cells. Europe saw the greatest deployment of high nickel cells in 2020 (predominantly NCM 6- and 7-Series), followed by China (dominated by NCM 8-Series) and the U.S. (high-nickel NCA).

Furthermore, nearly 30% of all passenger EV battery capacity deployed globally in 2020 was in the form of low nickel cells, such as NCM 1- to 5-Series cells. Last year, China saw the greatest deployment of low nickel cells globally, followed closely by Europe and at a distance by the U.S. In virtually all regions globally, the low nickel market is dominated by NCM 5-Series and to a lesser extent NCM 1-Series.

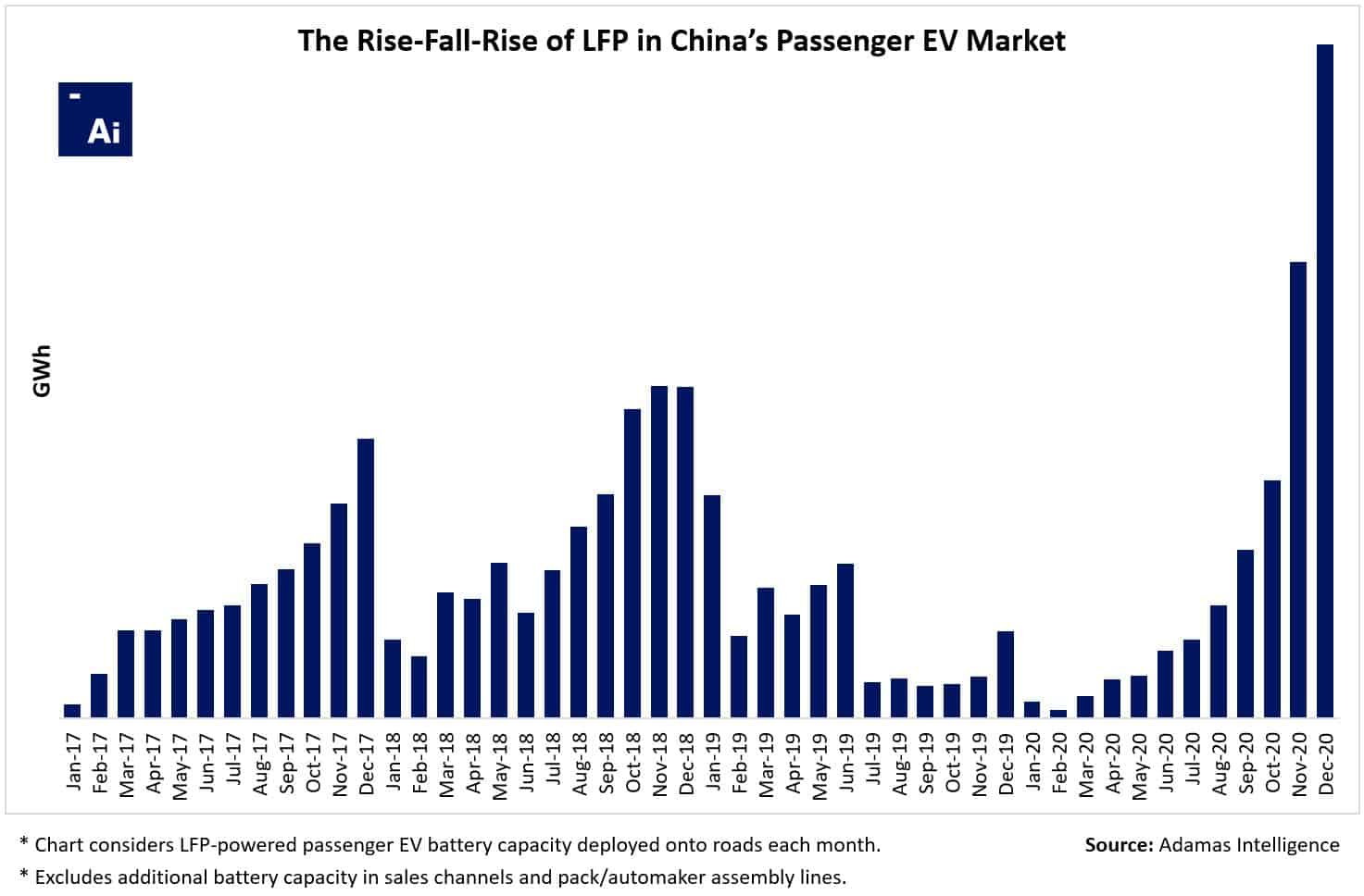

Lastly, in 2020 less than 10% of all passenger EV battery capacity deployed globally was in the form of no nickel cells, such as LFP and LMO/LTO. Not surprisingly, China saw the greatest deployment of no nickel cells globally in 2020 (predominantly LFP), followed by Europe and the U.S.

While LFP captured less than 10% of the passenger EV market last year by battery capacity deployed, it’s worth noting that this share reached as high as 11% in the fourth quarter of 2020 and we expect will edge closer to 15% by the middle of 2021.

Although unit sales of LFP-powered BEVs in China are rising like smoke, the sales-weighted average LFP-powered BEV in the nation has a battery pack capacity (in kWh) that is 51% lower than the sales-weighted average NCM 8-Series -powered BEV. As such, roughly speaking, the market needs to sell more than two LFP-powered BEVs for every one NCM/NCA-powered BEV sold for LFP to continue (re)capturing market share (by kWh deployed).