The European patient: Germany’s EV market takes the offramp

Eurozoned out

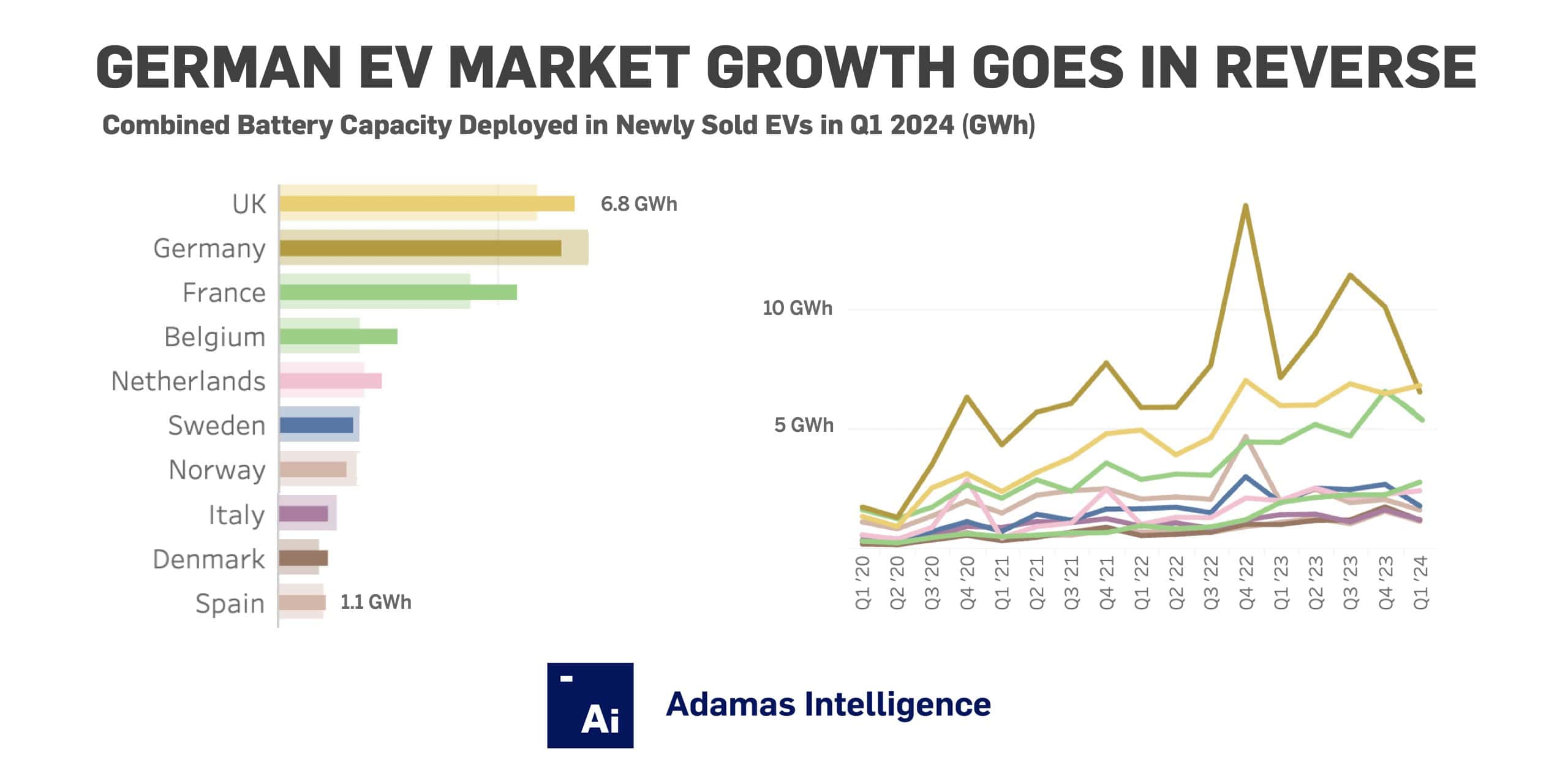

When measured in terms of GWhs of battery power rolled onto roads in newly sold vehicles (which provides a clearer picture of how fast the car parc is electrifying than sales alone), the global passenger EV market as a whole is in decent shape but key markets outside of China have hit a rough patch.

Worldwide, the combined EV battery capacity deployed in Q1 of this year, including plug-in (PHEVs) and conventional hybrids (HEVs), increased by nearly 24% year-over-year to 160.9 GWh.

At 82.6 GWh, Chinese EV buyers led the pack, rolling 34% more power-hours onto the country’s road in Q1 2024 than the same period last year. That compares to 23.9 GWh and 11% growth in the US, and a mere 8% expansion in Europe to 36.4 GWh.

Europe’s uninspiring first quarter came on the back of a pullback in some of its more mature markets including Norway and Sweden, where electric vehicle penetration rates already sit at 80% and 60% respectively, coupled with a sharp reversal in Italy where EVs have never ignited as much passion as internal combustion engined vehicles.

Rückwärts

But it is Germany, until now the world’s third largest EV market, that is most responsible for Europe’s current underperformance. The country saw a combined 6.5 GWh of fresh battery power hit autobahns during the first three months of the year. That’s down more than 8% from last year’s 7.1 GWh.

Conversely, the UK, which overtook Germany’s tally on a quarterly basis for the first time ever in Q1 2024, grew it electric car parc by 14% to 6.8 GWh, while France added 5.5 GWh, up 25% compared to the same period last year.

EVs made up 24% of total new EV registrations in Germany during Q1, the lowest rate since Q3 2020, while in the UK and France, respectively, 31% and 36% of all vehicles leaving showrooms were electrified. Exclude HEVs, which often have minimal or near non-existent electric-only range, and over four out of every five Germans steered clear of battery power.

Adamas take:

Made-in-China EVs (mainly non-Chinese brands including BMW, Dacia and Volvo) constituted just under 12% of all GWhs deployed in Germany during the first quarter of this year.

With the EU investigation into cheap Chinese EV exports to the bloc at an advanced stage and the imposition of tariffs thereafter almost a foregone conclusion, EV adoption in Europe – and Germany – will only encounter more roadblocks over the course of 2024.