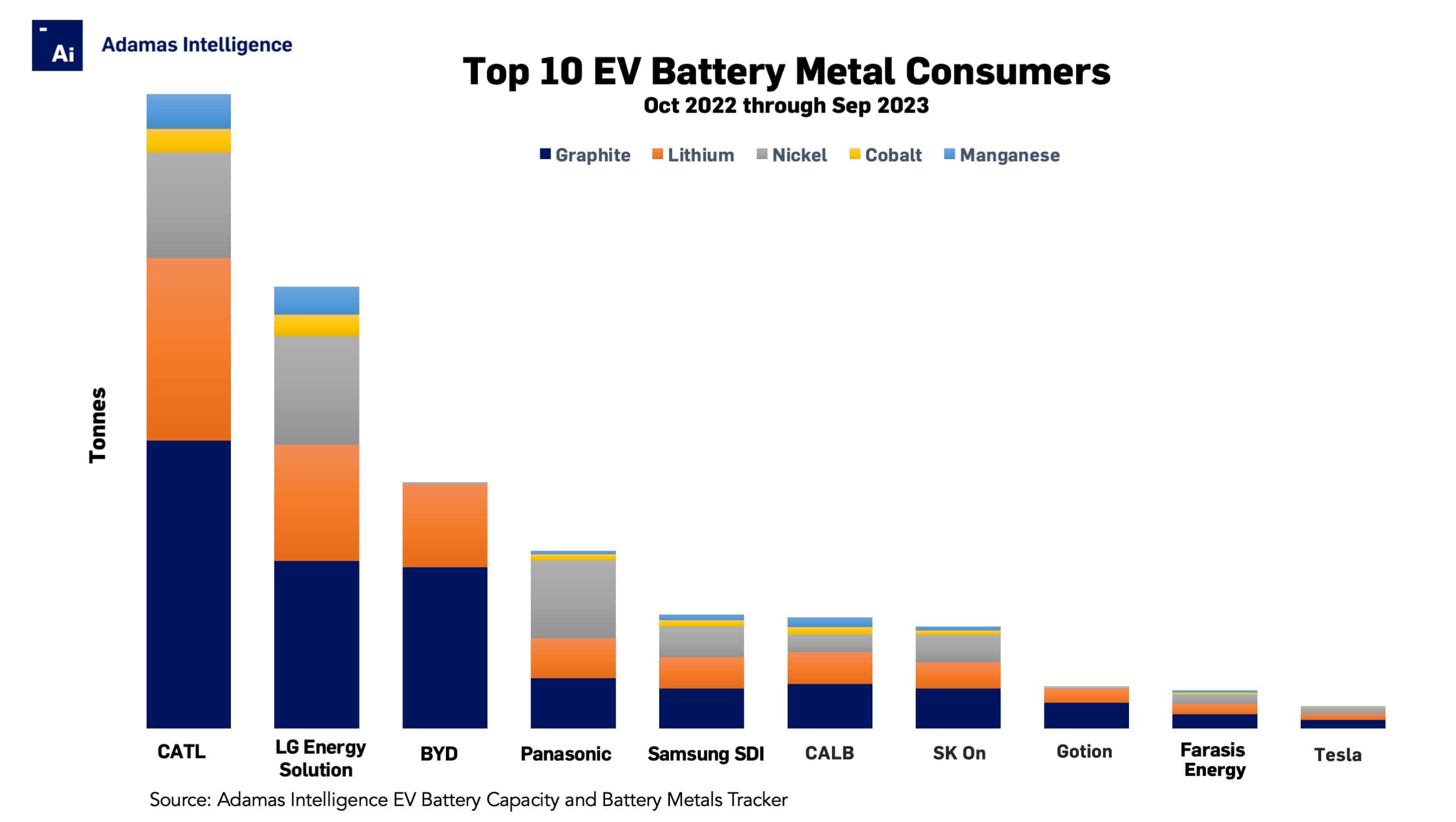

Top 10 EV battery metal consumers of the past 12 months

Trailing 12-month battery metals consumption scales 1m tonnes for the first time

In the past 12 months 1,357 kilotonnes of graphite, lithium, nickel, cobalt and manganese were contained in the batteries of electric vehicles sold around the world, a 45% jump over the 12 months prior.

The world’s number one EV cell manufacturer, Contemporary Amperex Technology Co Ltd, was responsible for 31% or 416kt of the total number of tonnes of battery metals deployed onto roads between October 2022 and September 2023.

CATL’s share of both lithium carbonate equivalent (LCE) and graphite deployed globally is 32% at 188kt and 120kt respectively.

The Fujian-based company used 69kt of nickel to manufacture the batteries in newly sold EVs over the past year affording it a lower, 26% share of the global total, a reflection of the fact that nickel-free LFP batteries and low nickel NCM 5-Series cells together account for more than 70% of its cell output.

CATL, worth over a $100 billion on the Shenzen stock exchange, commands 34% of battery manganese consumption (23kt in the past year) in the global EV supply chain, and its cobalt usage of 16kt represents 30% of the market.

Number two battery metal consumer LG Energy Solution is a buyer of 21% or 289kt of global battery metals entering the EV supply chain over the past year.

LG Energy Solution relies on high nickel cathode chemistries (NCM 6-Series and above) for over 90% of its cell production and nickel application at the company is higher than that of CATL at 71kt since October 2022.

LG Energy Solution, spun off from the South Korean conglomerate in 2020 in the biggest IPO ever on the Seoul stock market, used 14kt of cobalt (26% of the global total), 18kt of manganese (27%), 76kt LCE (20%) and 109kt graphite (19%).

Third-ranked auto and battery maker BYD has switched to LFP batteries for its entire range of vehicles and only applied a combined 1kt of nickel, cobalt and manganese in the batteries it supplies to a handful of customers, including US automaker Ford’s joint venture in China.

BYD, the world’s top EV make in 2023 when plug-in hybrids are included in the tally, at 54kt consumed 14% of the global total of graphite absorbed by electric cars over the 12-month period and 105kt of graphite for an 18% share.

Panasonic takes the no 4 slot among EV battery metal consumers garnering 9% of the global market (down from 22% in 2020). Over 116kt of nickel, cobalt, LCE, manganese and graphite were used in its batteries in newly sold EVs with Panasonic batteries during the period.

Panasonic’s battery nickel consumption represents 19% of the global EV market at 51kt, 4kt of cobalt translates to an 8% share and 2kt of manganese 3%. In LCE terms the company owns 7% of the market at 26kt and graphite use of 33kt equals a 6% market share over the last year.

The Japanese giant built its EV business in partnership with Tesla in a longstanding business relationship and today some 80% of its cell production is supplied to the Texas-based EV pioneer. Panasonic’s output is skewed towards nickel metal hydride batteries used in conventional hybrids. This and the third generation NCA batteries supplied to Tesla explains the Osaka-based company’s heavy nickel consumption.

Rounding out the top 5 is Samsung SDI, the battery unit of the Korean chaebol, which is responsible for 6% or 75kt of the world’s battery metal consumption over the past year.

Samsung SDI cells in the batteries of newly sold EVs contained 26kt of graphite, 20kt of LCE, 20kt of nickel, 4kt of cobalt and 3kt of manganese. Global share of manganese, graphite and LCE came in at 5% while nickel and cobalt applied constituted 8% and 9% of the global total respectively.

Samsung SDI edged out CALB and SK On for fifth position with the fast-growing Chinese battery maker applying 73kt of battery metals and the SK Innovation spin-off 67kt.

China’s Gotion and Farasis Energy occupies the number 8 and 9 slots with 28kt and 25kt respectively while Tesla’s cell business enters the top 10 for the first time on a trailing 12-month basis at 15kt of battery metals.

Adamas take:

Together the top 10 cell suppliers to the EV industry are responsible for more than 93% of the global consumption of battery metals on an annual basis. A testimony not just to the relative youth of the industry, but also the vast benefits scale brings to the material-intensive business of making electric cars.