Asia Pacific and Americas monthly car parc electrification rates fall to multi-year lows

Posts

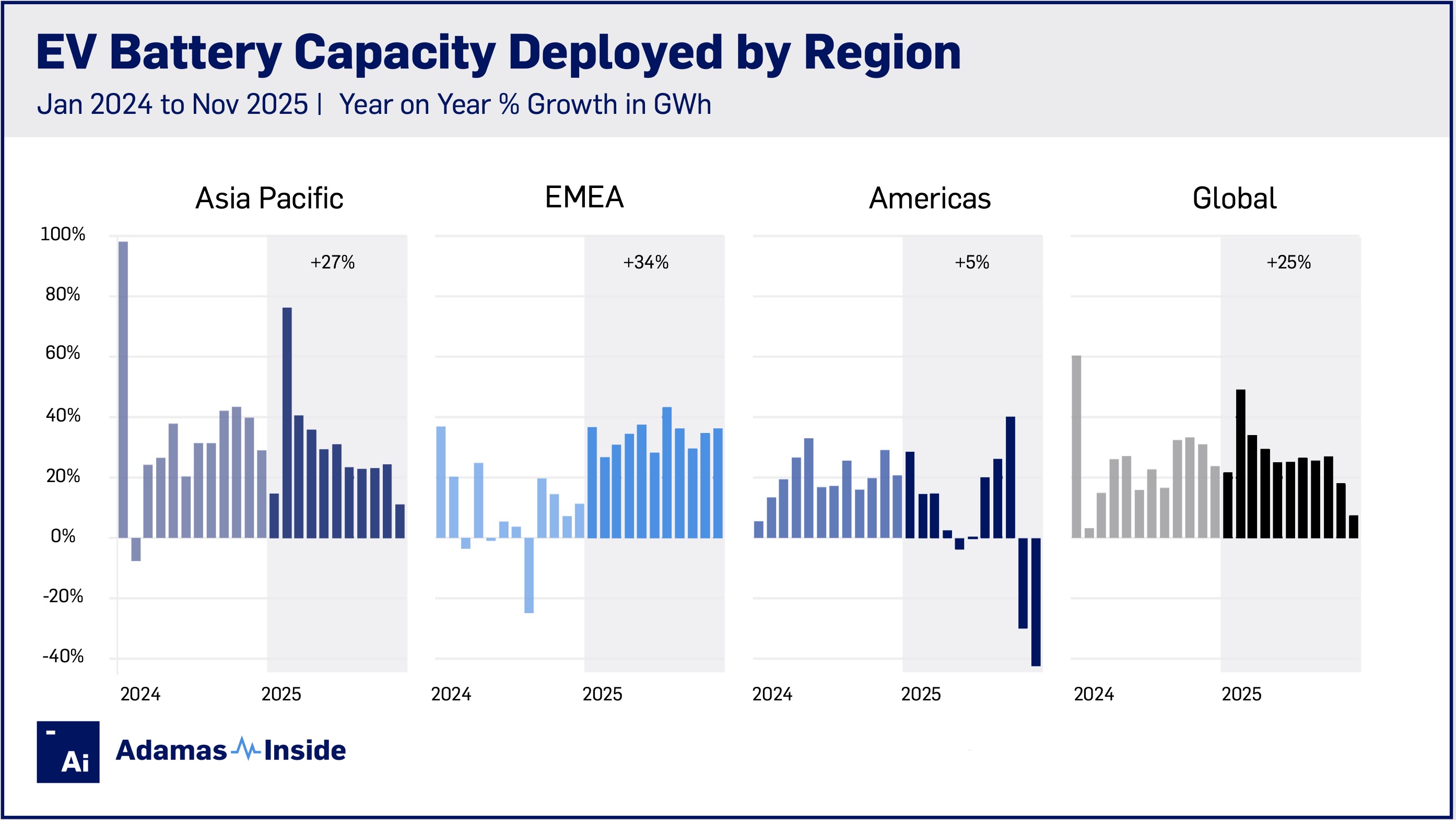

Over the first 11 months of 2025, 959.0 GWh of battery capacity was deployed onto roads globally in all newly sold passenger EVs combined, 25% more than the same period last year.

October and November 2025 came in just below the 100 GWh mark following September’s all-time record for global battery capacity deployment of 109.2 GWh.

Historically, December is the best month for global EV sales and 2025 is now likely to easily exceed the pivotal 1 TWh level for the first time, despite a marked slowdown in Asia Pacific in the second half of the year and a severe slump in the Americas following the withdrawal of US retail incentives at the end of September.

Asia-Pacific recorded 68.9 GWh deployed in newly sold EVs in November, the second best month in history for the region after the 70.0 GWh reached in October, but year-on-year growth of 11% was the weakest since the beginning of 2024.

The January-February deployment in the region is heavily affected by the timing of the Chinese lunar new year holidays. For instance, January 2024 saw year-on-year growth of 98%, while February that year saw a contraction, and last year the divergence was the other way around, as the graph illustrates.

Accounting for that means November was likely the weakest month in Asia Pacific for several years in terms of annual growth rates given the outsize role played by China, the world’s largest EV market by country mile.

Year to date, the region is still showing solid growth with regional deployment from January through November 2025, up 27% year on year to a total of 612.1 GWh. Asia Pacific accounted for a full 64% of global battery capacity deployment over the 11-month period.

European EV buyers rolled 20.7 GWh of fresh battery capacity onto regional roads in November, representing a nearly 32% jump year over year. After a choppy 2024, European growth has been consistently strong in 2025, and year-to-date the region has expanded by 31% to 192.0 GWh. One out of every five GWh added to the global EV parc this year has been in continental Europe, the British Isles and Russia.

When adding the still small (2% of the global total) but fast-growing Middle East and Africa market, year-on-year growth rose by 34% to 213.6 GWh as per the accompanying graph. In the Middle East and Africa, the November deployment rose 54% to 2.2 GWh from the same month in 2024, marking the slowest year-on-year growth since February. From January through November last year, the region expanded by 69% to 21.6 GWh.

In the Americas, battery capacity deployed continued to fall, and at only 8.2 GWh, November was the worst month in GWh terms since February 2023. In the US, the November total was the lowest since August 2022 and almost half that of the same month in 2024. US weakness dragged down regional growth to less than 5% year to date, bringing the 11-month total to 133.3 GWh.

Contact the Adamas team to learn more or check out the intelligence services below.