China vs ex-China: A tale of two very different outlooks for rare earths

When discussing the outlook for rare earths supply and demand, it can be a mistake to extrapolate a single outlook onto all regions globally. In the case of China versus the ex-China market, we continue to see a tale of two very different outlooks unfolding over the medium- to long-term.

China to increasingly import ex-China surpluses

When discussing the outlook for rare earths supply and demand, it can be a mistake to extrapolate a single outlook onto all regions globally. In the case of China versus the ex-China market, we continue to see a tale of two very different outlooks unfolding over the medium- to long-term.

For China, as the world’s largest producer of NdFeB magnets, we expect the nation will increasingly import surplus rare earth concentrate and oxide production from the rest of the world in an attempt to satisfy growing demand from domestic magnet makers.

As global rare earth supply struggles to keep up with global demand through the latter half of the forecast period we expect it will be China’s magnet makers – responsible for the vast majority of global production – that bear the brunt of the shortages if they cannot secure the rare earth inputs they need.

Conversely, for the ex-China world, we project collective overproduction of rare earth oxides into the foreseeable future as mine production grows substantially faster than ex-China magnet production, an issue exacerbated by insufficient midstream capacity to convert oxides into metals and alloys needed to produce magnets.

As such, we foresee a future where China grows increasingly reliant on foreign sources of supply, leading the balance of pricing power to tilt gradually more towards the ex-China market.

Should China’s production not increase substantially more than expected in the next decade, we foresee a pervasive shift towards seller’s market conditions that ex-China suppliers can look to capitalize on.

On the contrary, in the ex-China market, we foresee a gradual shift towards buyer’s market conditions, ultimately incentivizing exports to China first and foremost.

All things considered, we expect the early 2030s will see a turning point in which China halts exports of NdPr oxide, Dy oxide and Tb oxide and increasingly imports surplus supplies from the rest of the world.

Demand from magnet integrators vs magnet markers

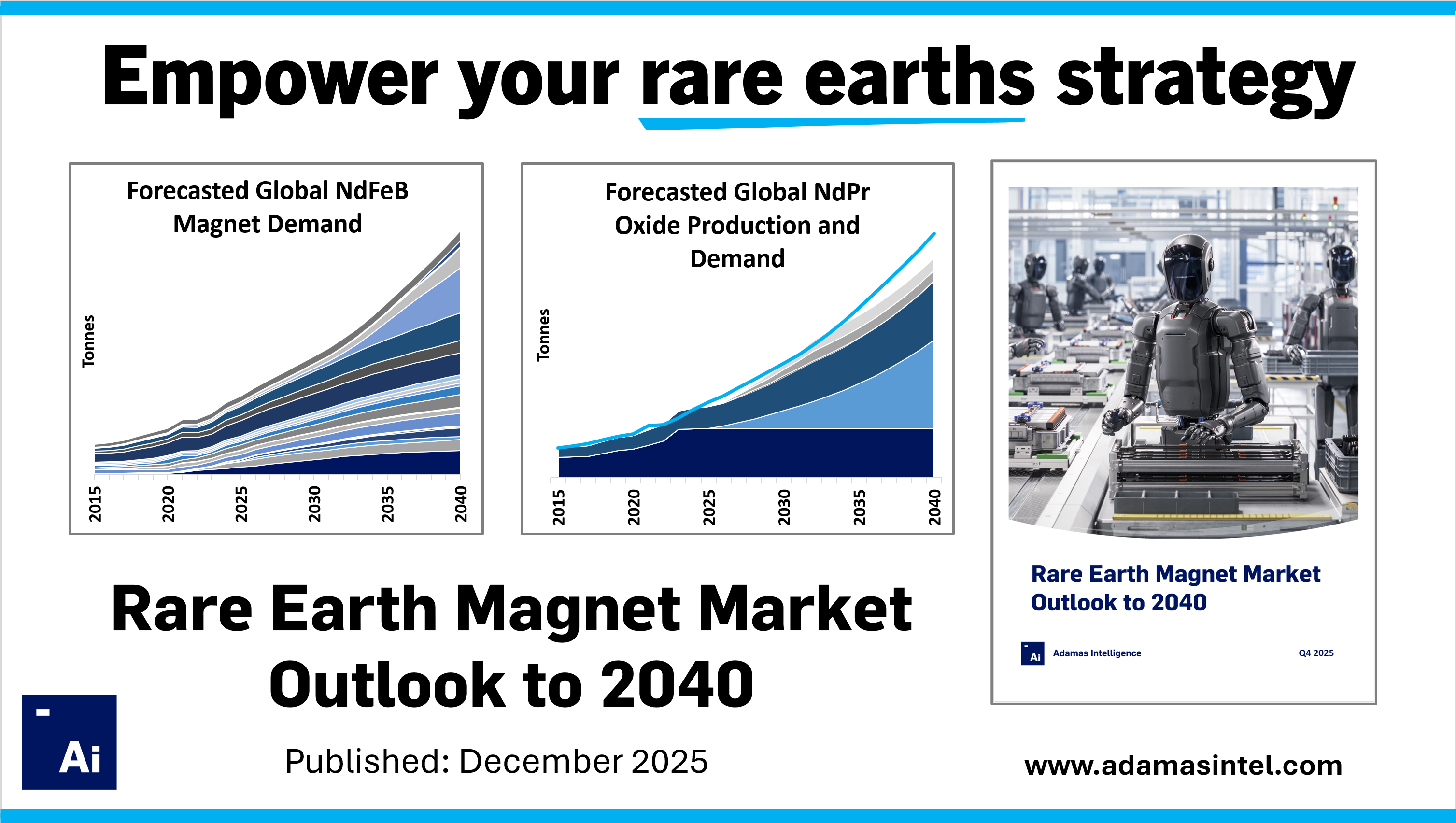

From 2025 through 2040, we forecast that China’s production of NdPr oxide will be sufficient to meet demand from magnet integrators (“MI”) in the country (i.e., companies that buy magnets to integrate them into parts and finished products; shown by the red line) but will be insufficient to meet demand from magnet makers (“MM”) in the country (i.e., companies that use didymium to produce NdFeB for domestic integrators and for export to foreign integrators; shown by the blue line), necessitating the import of foreign supplies to fill the gap.

Conversely, from 2025 through 2040, we forecast that production of NdPr oxide outside China (“ex-China”) will exceed demand from magnet makers ex-China (blue line), yielding surpluses that could be exported to China if ex-China magnet production capacity does not exceed expectations.

However, as shown by the red line on the figure above, ex-China demand for NdPr oxide in NdFeB magnets by ex-China magnet integrators exceeds what ex-China magnet makers are expected to deliver, shown by the blue line, necessitating magnet imports from China to fill the gap, or a major increase in ex-China magnet production to make full use of ex-China NdPr oxide supplies.

As it stands today, the upstream rare earth supply chain ex-China is positioning to capitalize on the full extent of demand from ex-China magnet integrators, however, unless ex-China magnet production increases beyond expectations, magnet production capacity will present a bottleneck.

Currently, the ex-China pipeline of existing, under construction and planned production capacity has potential to exceed 80,000 tonnes of NdFeB magnets per annum by 2030, which, if realized, would help to minimize the gap between blue and red lines by 2030, but would risk experiencing NdPr oxide shortages thereafter if ex-China supplies are not substantially boosted beyond expectations.

A must-have resource for anyone with a professional interest in the mine-to-magnet supply chain

Empower your organization to seize opportunities and navigate risks with the latest, most comprehensive industry analysis, market data and forecasts available.

Our new Rare Earth Magnet Market Outlook to 2040 report is a must-have resource for project developers, miners, processors, metal makers, magnet makers, end users, institutional investors, government agencies and other stakeholders with a professional interest in the mine-to-magnet supply chain.

Contact us for more information about the new report and our other industry-leading services.